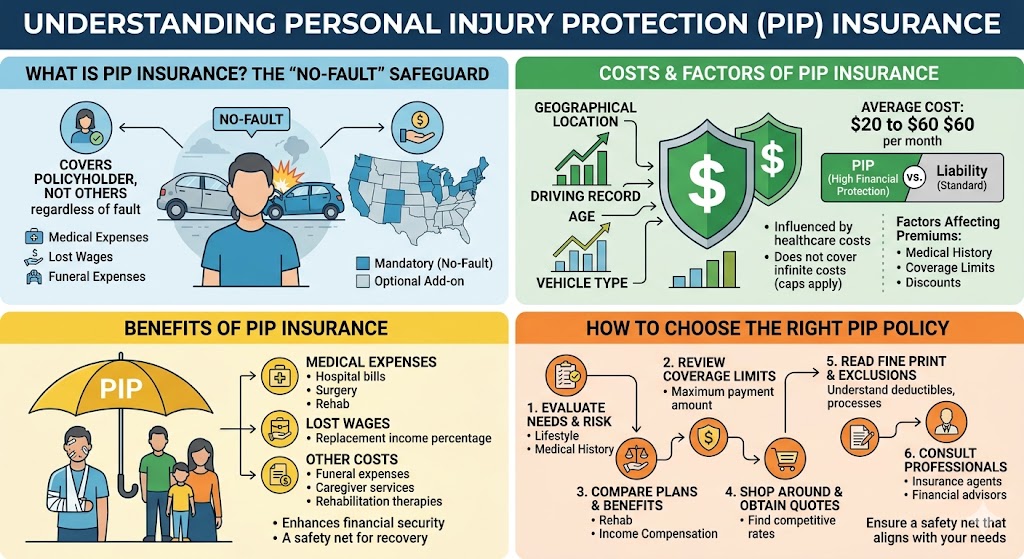

Personal Injury Protection (PIP) insurance is a type of auto insurance that provides coverage for medical expenses and, in some cases, lost wages and other related costs that arise from injuries sustained in an automobile accident. Unlike standard liability insurance, which covers damages to other parties in an accident, PIP is designed to cover the policyholder’s expenses, regardless of fault. This can include hospital bills, rehabilitation costs, and even funeral expenses in the unfortunate event of a fatality.

One of the key features of PIP insurance is its no-fault nature. This means that, in most cases, individuals can receive benefits from their own PIP policy without having to establish liability or prove that the other party was at fault. This advantage can expedite the claims process and ensure that injured parties receive necessary medical care promptly. However, the specific benefits offered under PIP can vary significantly across different states.

In terms of legal requirements, PIP insurance is mandatory in some states, categorized as ‘no-fault’ states. In these locations, drivers are required to carry a minimum level of PIP coverage. Other states offer PIP as an optional add-on to standard auto insurance policies. Individuals living in states where PIP is not mandatory may still consider obtaining it for the financial protection it provides against unforeseen medical expenses following an accident.

Ultimately, understanding PIP insurance means recognizing its critical role within the broader spectrum of auto insurance. It serves as a necessary safeguard for motorists, ensuring that they are financially protected in the event of an accident. By comprehensively assessing the various policies available, drivers can make informed decisions that best suit their needs and circumstances.

Costs of PIP Insurance

Personal Injury Protection (PIP) insurance serves as a fundamental layer of coverage in the realm of auto insurance, particularly designed to cover medical expenses related to automobile accidents. Understanding the costs of PIP insurance is crucial for both existing and potential policyholders. On average, the cost of PIP insurance can vary significantly based on various factors such as geographical location, driving record, age, and even the type of vehicle insured. In some states, PIP is mandatory, which can influence the average premium rates across the board.

For instance, states with higher healthcare costs may see elevated PIP premiums, while safer driving environments could lead to lower costs. On average, drivers can expect to pay between $20 to $60 per month for PIP coverage. When compared to other types of auto insurance, such as liability insurance, PIP may often seem more expensive; however, it significantly enhances financial protection.

Moreover, certain factors may contribute to the fluctuation of PIP premiums. These factors include the insured’s medical history, the chosen coverage limits, and any discounts that may apply. It is essential to assess these variables thoroughly to arrive at the most cost-effective solution.

It’s important to note that while PIP covers a wide range of expenses, there are certain out-of-pocket costs that may not be included. For example, PIP generally does not cover lost wages after a specific threshold or any long-term care requirements that may arise out of an incident. Therefore, it is advisable for individuals to evaluate their specific needs, considering both the costs of PIP and any additional coverage required, to ensure comprehensive financial protection in the event of an accident.

Benefits of Having PIP Insurance

Personal Injury Protection (PIP) insurance serves as a valuable financial resource for individuals involved in automobile accidents. One of the most significant benefits of holding a PIP policy is that it covers medical expenses that may arise from injuries sustained in an accident. This coverage typically includes hospital bills, surgeries, rehabilitation costs, and other medical treatments that can be financially burdensome. Given the often high cost of medical care, having PIP can mitigate financial stress during recovery.

In addition to medical expenses, PIP insurance also provides coverage for lost wages. If an injured person is unable to work due to their injuries, PIP can help replace a percentage of their lost income. This benefit is particularly crucial, as it ensures that individuals can maintain their financial obligation during a challenging period when earnings may be compromised.

Moreover, PIP insurance can include coverage for other associated costs, such as funeral expenses in the unfortunate event of a fatal accident and services provided by caregivers. Many PIP policies also offer coverage for rehabilitation therapies, which can be essential for individuals recovering from serious injuries. This comprehensive nature of PIP insurance ensures that various aspects of recovery are accounted for, providing a safety net that is often not addressed by traditional health insurance alone.

In summary, having Personal Injury Protection insurance can greatly enhance the financial security of policyholders involved in vehicle accidents. By covering medical expenses, lost wages, rehabilitation, and other related costs, PIP insurance plays a crucial role in helping individuals manage the aftermath of potentially life-altering incidents.

How to Choose the Right PIP Policy

Selecting the appropriate Personal Injury Protection (PIP) policy is crucial for ensuring adequate coverage in the event of an accident. The first step is to evaluate your current needs and circumstances. It is essential to consider various factors, such as your lifestyle, medical history, and the types of activities you frequently engage in. For instance, if you participate in high-risk activities or have pre-existing health conditions, opting for a policy with higher coverage limits can provide enhanced financial security.

Coverage limits refer to the maximum amount that an insurance company will pay under the policy. Understandably, higher limits often correlate with higher premiums, but assessing your potential medical expenses and lost wages can justify this investment. Review the different PIP plans available, comparing their benefits and coverage options. Some insurers may offer supplementary services, such as rehabilitation costs and lost income compensation, which can significantly influence your decision.

Moreover, it is vital to shop around and obtain quotes from various insurance providers. This process will not only help identify competitive rates but also allow you to understand the nuances of each policy. Pay close attention to the fine print; terms and conditions can differ substantially across policies. Ensure you comprehend the exclusions, deductibles, and claim processes as they can significantly affect your coverage experience.

Another critical aspect is to consult with insurance agents or financial advisors. These professionals can provide valuable insights tailored to your unique situation, further assisting in your decision-making. By meticulously considering these factors and utilizing available resources, you can make an informed choice regarding your PIP insurance policy, ultimately ensuring a safety net that aligns with your needs.