Navigating healthcare is confusing enough without a side order of financial alphabet soup. If you’re staring at your open enrollment options trying to figure out the difference between an HSA (Health Savings Account) and an FSA (Flexible Spending Account), you are definitely not alone.

Both accounts let you pay for medical expenses like prescriptions, doctor visits, and even daily essentials using pre-tax dollars. But while they sound nearly identical, they behave in completely opposite ways. Picking the wrong one can mean missing out on major tax breaks—or worse, watching your hard-earned money vanish.

Let’s break down the rules in plain English so you can choose the right account for your life and your wallet.

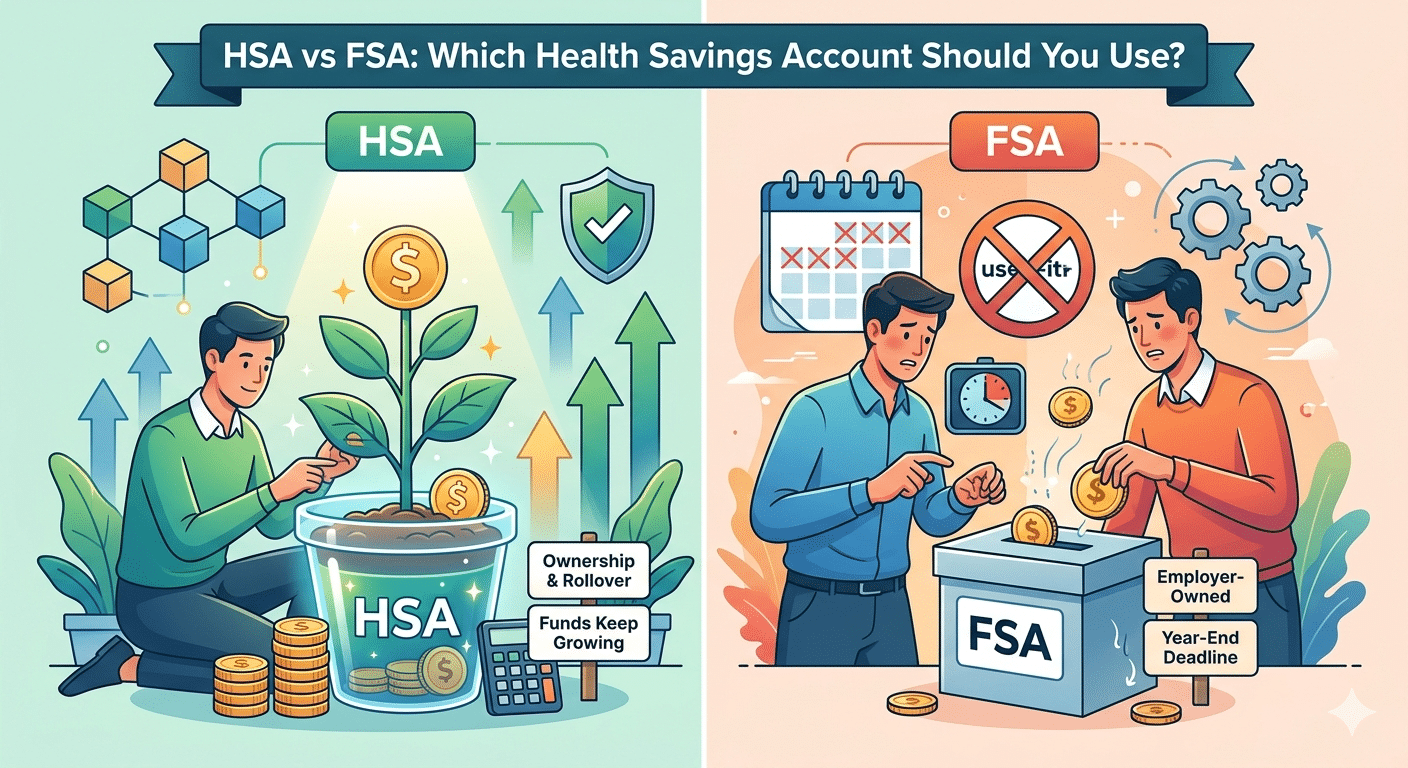

The HSA: The Ultimate Long-Term Nest Egg

Think of a Health Savings Account (HSA) like a personal retirement account specifically for your health.

To qualify for an HSA, you must be enrolled in a High-Deductible Health Plan (HDHP). Because these insurance plans have lower monthly premiums but higher out-of-pocket costs when you get care, the government created the HSA to help you save for those upfront expenses.

The magic of the HSA lies in its “triple tax advantage”:

-

The money goes into your account pre-tax.

-

It grows entirely tax-free through interest or investments.

-

You pay zero taxes when you withdraw it for qualified medical costs.

Best of all? The money is yours forever. It never expires. If you change jobs, it moves with you. If you don’t spend it this year, it rolls over to the next. You can even invest your balance in mutual funds or stocks, letting it compound over decades to fund your healthcare in retirement.

The FSA: The “Use-It-or-Lose-It” Helper

A Flexible Spending Account (FSA) is an employer-sponsored perk, and it works a bit differently. You don’t need a specific high-deductible health plan to use one; you can pair an FSA with traditional insurance plans like a PPO or HMO.

During open enrollment, you decide how much you want to contribute for the upcoming year, and that amount is sliced out of your paychecks pre-tax.

The biggest catch with an FSA is the infamous “use-it-or-lose-it” rule. The cash you put into an FSA is meant to be spent within that specific calendar year. While some employers offer a short grace period or allow you to roll over a tiny fraction of the funds, any leftover money generally gets swallowed by your employer at the end of the year.

HSA vs. FSA: The Core Differences

| Feature | Health Savings Account (HSA) | Flexible Spending Account (FSA) |

| Who Owns It? | You do. It’s entirely portable. | Your employer. Leave the job, lose the funds. |

| Do Funds Expire? | Never. They roll over indefinitely. | Yes. Spend it by year’s end or lose it. |

| Can I Invest It? | Yes, like a retirement account. | No, it sits as cash. |

| Plan Requirement | Must have a High-Deductible Plan (HDHP) | Works with most traditional plans. |

Which Account Wins for You?

The right choice usually comes down to your current health insurance plan and how predictably you spend money on medical care.

Go with an HSA if:

-

You want a long-term investment tool: If you can afford to pay for minor medical bills out of pocket and let your pre-tax HSA contributions grow, it becomes a powerful secondary retirement vehicle.

-

You prefer lower monthly premiums: If you are generally healthy and choose an HDHP to save on monthly premium costs, the HSA is your safety net.

Go with an FSA if:

-

You have predictable yearly medical costs: If you know you have an upcoming surgery, regular therapy appointments, or expensive monthly prescriptions, an FSA lets you pay for those guaranteed costs with a massive tax discount.

-

You prefer standard insurance: If you feel safer with a low-deductible PPO or HMO plan, the FSA is your go-to option for tax-advantaged medical savings.

The Bottom Line

If you have a high-deductible plan and want maximum flexibility and long-term wealth building, the HSA is arguably one of the best financial accounts available. But if you prefer traditional health insurance and can accurately budget your health costs for the next 12 months, an FSA will give your budget a welcome tax break. Take a look at last year’s medical receipts, check your insurance plan, and pick the tool that gives you the most peace of mind.