A story millions of Americans are living right now.

Marcus had done everything right. He’d paid off his student loans, built up his savings, and landed a stable job earning $65,000 a year. At 31, he felt ready for the next chapter — homeownership. But when he opened his laptop and started browsing listings, reality hit fast.

“How much house can I actually afford?” he typed into Google at 11 p.m., a cup of cold coffee beside him.

If you’ve ever sat in Marcus’s shoes, this article is for you.

Starting With the Numbers: What $65,000 Really Means

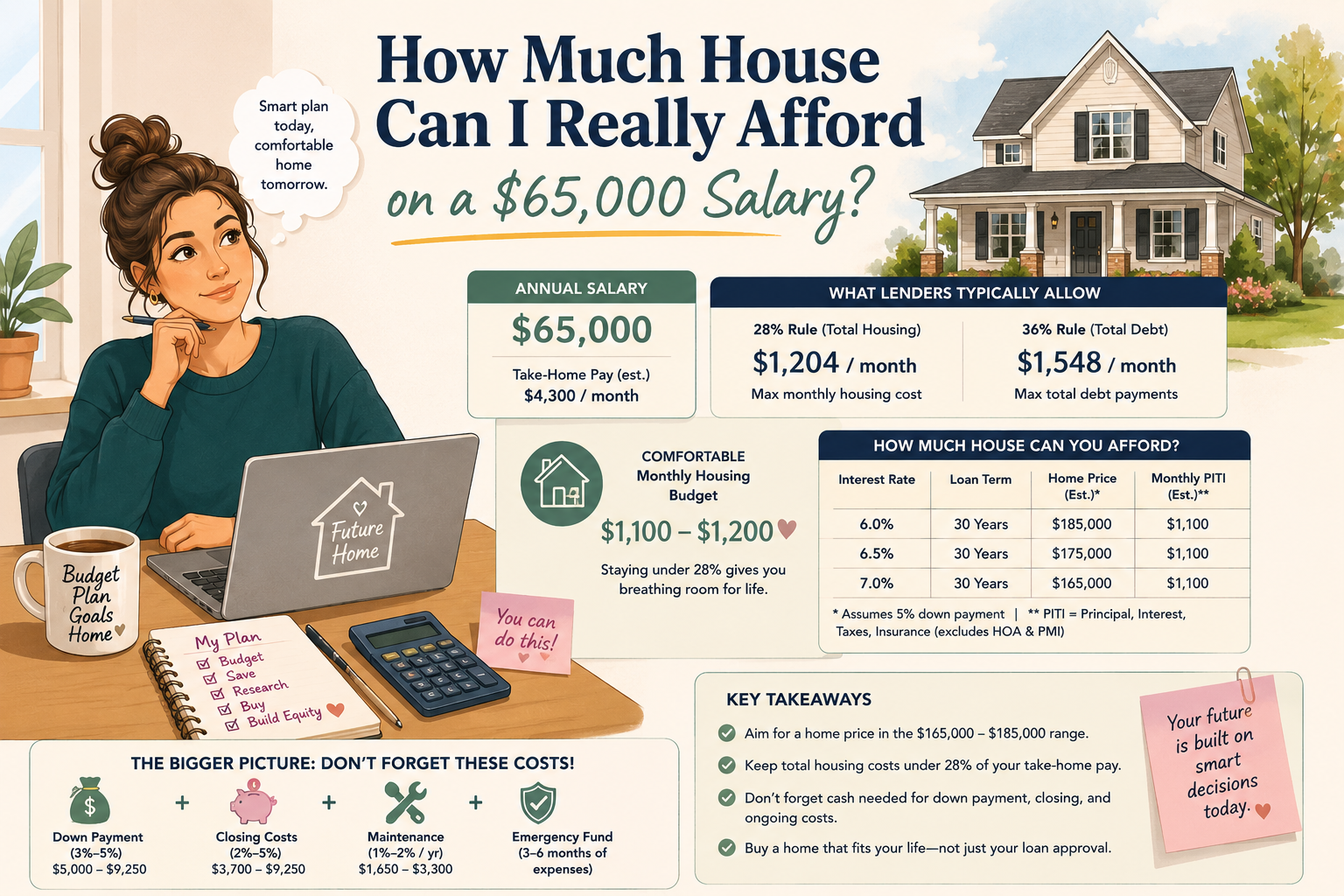

A $65,000 annual salary breaks down to roughly $5,417 per month before taxes. After federal and state taxes, you’re likely taking home somewhere between $4,000 and $4,500 per month — depending on your state and deductions.

That number is your foundation. Everything else builds from it.

The Golden Rule of Home Affordability

Most financial experts follow the 28/36 rule:

- Spend no more than 28% of your gross monthly income on housing costs (mortgage, taxes, insurance).

- Keep total debt — including car loans, student loans, and credit cards — under 36% of gross income.

For a $65,000 salary, 28% of your $5,417 gross monthly income equals about $1,517 per month for housing.

That’s your target mortgage payment ceiling.

So What Home Price Does That Translate To?

Marcus ran the math — and so can you.

With a 20% down payment, a 30-year fixed mortgage, and today’s average interest rates hovering around 6.5–7%, a monthly payment of $1,500 supports a loan of roughly $225,000 to $235,000.

Add a 20% down payment of around $50,000–$55,000, and the total home price lands near $275,000–$290,000.

That’s a realistic ballpark for a $65,000 earner — but the story doesn’t end there.

The Hidden Costs That Change Everything

Marcus almost made the mistake of stopping at the mortgage payment. His lender reminded him of the costs that don’t make the headlines:

- Property taxes (1–2% of home value annually)

- Homeowner’s insurance (~$150/month on average)

- Private Mortgage Insurance (PMI) if your down payment is under 20%

- HOA fees, if applicable

- Maintenance and repairs — experts recommend budgeting 1% of home value per year

These costs can easily add $400–$700 per month to your true housing expense. Factor them in before you fall in love with a listing.

Your Credit Score Is a Game-Changer

Two buyers with the same $65,000 salary can end up with very different mortgages — simply because of their credit scores.

A score above 740 can unlock interest rates nearly 1–1.5% lower than a score in the 620s. Over a 30-year mortgage, that difference can cost — or save — tens of thousands of dollars.

Marcus spent six months improving his score before applying. It was worth every month of patience.

Location Changes the Entire Equation

A $275,000 budget buys a spacious three-bedroom home in Columbus, Ohio or San Antonio, Texas. In San Francisco or Seattle? It barely covers a parking spot.

Your local market matters enormously. Research median home prices in your target area and adjust expectations accordingly. Sometimes, expanding your search radius by just 15–20 miles can dramatically increase what your budget can buy.

The Real Answer to Marcus’s Question

He could afford a home in the $250,000–$290,000 range — comfortably, without stretching himself dangerously thin. He bought a $265,000 townhouse, put 20% down, and kept his monthly housing cost at $1,480.

The lesson? Affordability isn’t just about what a bank will approve you for. It’s about what lets you sleep at night, save for retirement, and still enjoy your life.

On a $65,000 salary, homeownership is absolutely within reach — if you do the math honestly and buy with your head, not just your heart.

Ready to run your own numbers? Use a mortgage calculator, talk to a HUD-approved housing counselor, and take your time. The right home is out there — and it fits your budget.