Imagine finding your dream home, calculating your monthly mortgage payments, and realizing you can comfortably afford the down payment. You are ready to sign the papers and move in. But then, your real estate agent hands you a document detailing the final cash needed to close—and it is thousands of dollars higher than you expected.

When buying a home, most first-time buyers focus entirely on the purchase price and the down payment. However, the true cost of homeownership includes a hidden layer of upfront fees, administrative charges, and immediate maintenance expenses.

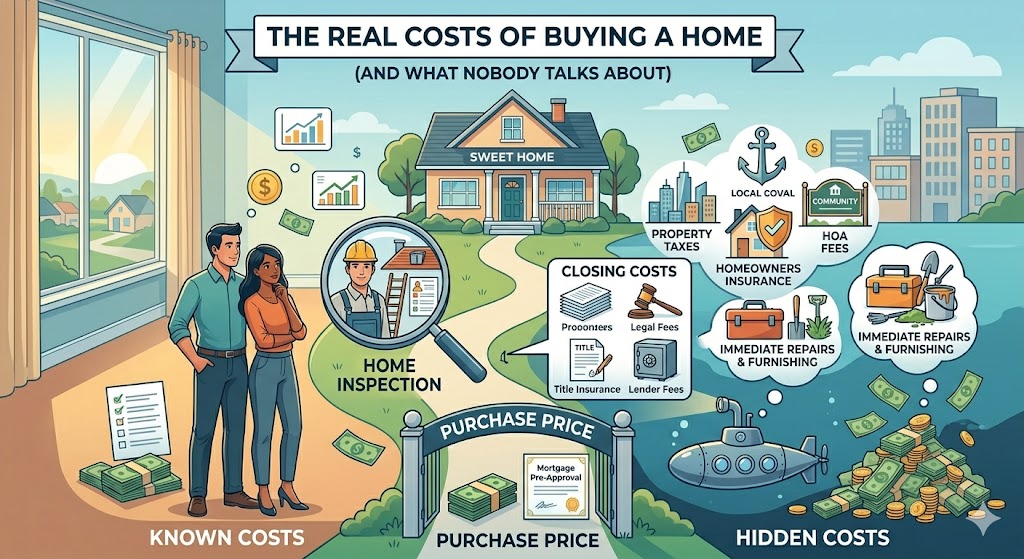

To avoid a financial shock at the closing table, you need to look past the sticker price. Here are the real costs of buying a home that nobody talks about.

1. Closing Costs: The 2% to 5% Surprise

Closing costs are the processing fees you pay to your lender and various third parties to finalize your mortgage. As a general rule of thumb, closing costs typically range between 2% and 5% of the total home loan amount. If you are buying a $400,000 home, that means you could need an extra $8,000 to $20,000 in cash on closing day, entirely separate from your down payment.

These costs are comprised of dozens of smaller line items, including:

-

Loan Origination Fees: What the lender charges to evaluate and process your loan application.

-

Title Insurance and Search Fees: Paid to a title company to ensure the seller legally owns the property and that there are no outstanding liens (unpaid debts) against it.

-

Appraisal Fees: Lenders require a professional appraisal (usually costing $300 to $600) to confirm the home is actually worth the amount you are borrowing.

2. The Multi-Layered Inspection Phase

A standard home inspection is a non-negotiable step to protect your investment. A general inspector checks the roof, foundation, plumbing, and electrical systems, usually costing between $300 and $500.

However, a general inspection only scratches the surface. Depending on the age and location of the home, you may need specialized inspections that quickly add up:

-

Termite/Pest Inspection: $100 – $200

-

Radon Testing: $150 – $300

-

Sewer Scope (checking the main line for cracks or tree roots): $250 – $400

-

Mold or Lead Paint Testing: $300+

Skipping these can save you a few hundred dollars today but cost you tens of thousands later if structural or environmental issues are left undetected.

3. Property Taxes and Insurance Prepaids

Lenders do not like taking risks. To ensure your asset is protected, they often require you to pay a portion of your homeowners insurance and property taxes upfront at closing.

This money goes into an escrow account—a neutral holding account managed by your lender. You might be asked to fund up to a year’s worth of homeowners insurance and several months of property taxes in advance, which can add thousands to your out-of-pocket closing expenses.

4. Immediate Moving and “Day-One” Expenses

The costs do not stop once you get the keys. Moving itself is a major expense. Hiring professional movers can cost anywhere from $1,000 to over $5,000 for long-distance transitions.

Furthermore, first-time homeowners routinely underestimate “Day-One” expenses. Buying a larger space often means purchasing new furniture, window treatments, and lawn care equipment. There are also utility hookup fees, smart lock replacements for security, and minor immediate repairs (like fresh paint or carpet cleaning) that you will want to tackle before your furniture arrives.

The Golden Rule: When budgeting for a home, never empty your bank account for the down payment. Always maintain an emergency fund of at least 3 to 6 months of living expenses after all closing and moving costs are paid.

By understanding these hidden expenses early in your house hunt, you can budget realistically, negotiate smarter, and step into your new home with financial confidence rather than financial stress.