Five years ago, I sat at my kitchen table with two laptops open, three tabs of conflicting financial advice, and a cold cup of tea. I had finally built up my emergency fund, and I knew it was time to take the next step: investing.

But as I stared at acronyms like ETF, NAV, and expense ratios, my confidence evaporated. The financial world felt like an exclusive boys’ club, intentionally designed to speak in a language I didn’t understand. I felt paralyzed by the fear of making the “wrong” choice and losing my hard-earned money.

What I didn’t know then is that the best investing strategy for long-term wealth building doesn’t require a degree in finance. It usually comes down to a simple, powerful showdown: Index Funds vs. Exchange-Traded Funds (ETFs).

Historically, women face unique financial hurdles—we live longer, experience the gender wage gap, and often take career breaks for caregiving. This makes investing early and efficiently non-negotiable for our future autonomy. If you are ready to make your money work as hard as you do, here is the stress-free breakdown of what every woman needs to know before diving in.

The Core Concept: What Are They, Anyway?

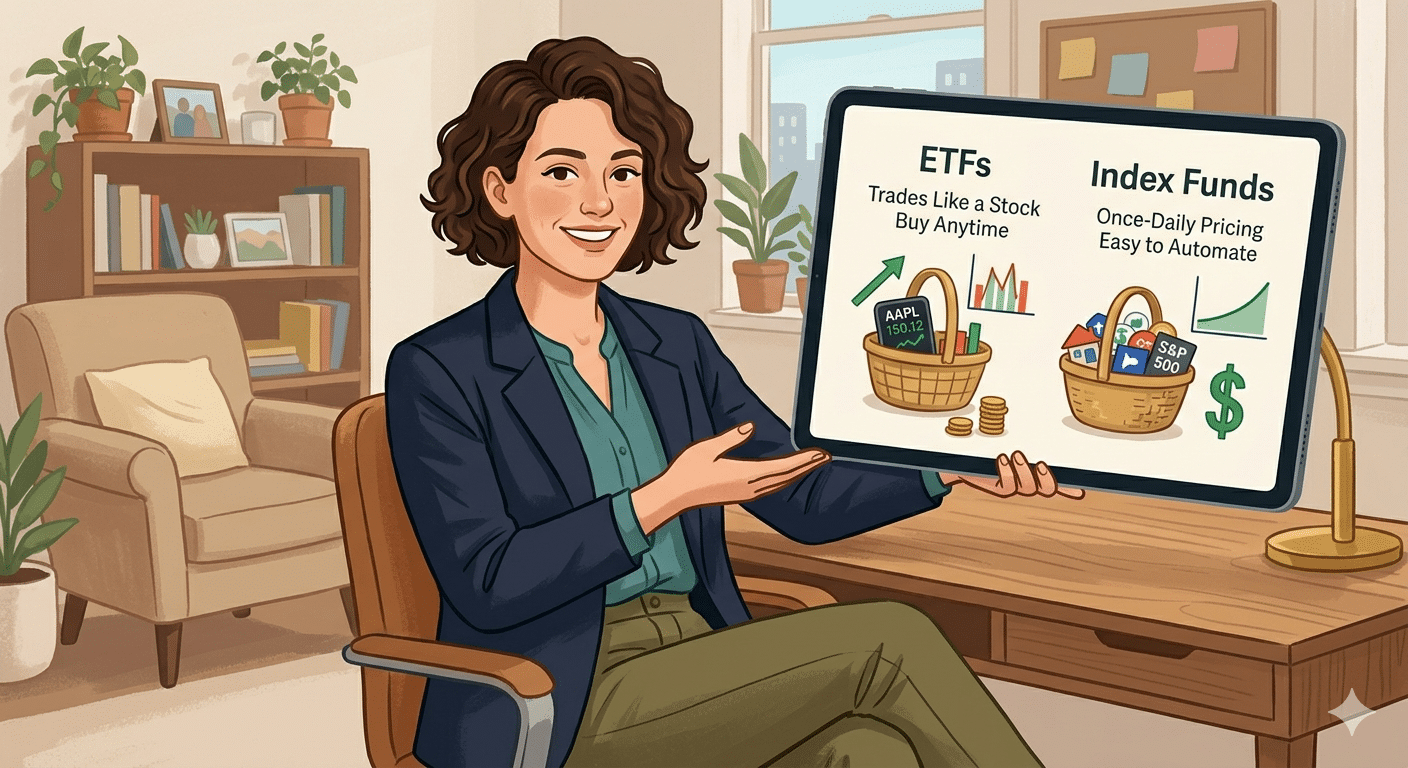

Before looking at the differences, it helps to understand what these two vehicles have in common. Think of both index funds and ETFs as financial gift baskets.

Instead of buying a single share of one company (like Apple or Amazon)—which is incredibly risky if that one company hits a rough patch—you buy a basket that contains tiny pieces of hundreds of different companies. If one company in the basket fails, the others are there to balance it out.

Both index funds and ETFs track a specific “index,” like the S&P 500, which represents the 500 largest companies in the US. By buying either one, you are essentially betting on the long-term growth of the entire economy rather than trying to pick individual winners.

The Key Differences That Matter to Your Wallet

While they hold similar ingredients, the way you buy, sell, and manage these baskets differs.

1. How They Trade (Flexibility vs. Simplicity)

-

ETFs: These trade exactly like individual stocks on an exchange. This means their prices fluctuate second by second throughout the trading day. You can buy or sell them at 10:00 AM, 1:30 PM, or right before the market closes.

-

Index Funds: These are a type of mutual fund. They only price once a day, after the stock market closes at 4:00 PM. No matter what time of day you place your order, everyone gets the exact same price at closing.

2. The Minimum Investment Barrier

-

ETFs: You can usually start investing with the price of just a single share—or even less if your brokerage allows fractional shares. If a share costs $50, you can start with $50.

-

Index Funds: Traditional index funds often require a minimum initial investment to get through the door, sometimes ranging from $1,000 to $3,000.

3. Automation (The Ultimate Sanity Saver)

-

Index Funds: Because they price once a day, index funds are incredibly easy to automate. You can set your account to automatically pull $100 from your checking account every payday and invest it straight into the fund without lifting a finger.

-

ETFs: Because they trade like stocks, automating them can sometimes be slightly more complicated depending on your brokerage platform, though many modern platforms are closing this gap.

Which One is Right for You?

Choosing between the two depends entirely on your personal style and financial behavior.

If you love the idea of set-it-and-forget-it investing—where you automate a monthly contribution and never look at the stock market tickers—Index Funds are your best friend. They prevent you from trying to “time the market” because you are building wealth steadily in the background.

If you are starting with a smaller chunk of cash and want total flexibility to move your money around instantly, ETFs are an incredible, low-cost gateway into building real wealth.

The Ultimate Rule: Just Start

The night I finally closed those confusing tabs, I picked a simple, low-cost ETF and invested my first $100. Watching that number grow over the years completely changed my relationship with money.

Don’t let the jargon intimidate you or keep you on the sidelines. Whether you choose an index fund or an ETF, the most important step is simply getting your money into the market so compound interest can start working its magic for your future.