Your mortgage statement arrives every month, but do you actually understand what’s inside it? Most homeowners glance at the payment due and move on — but buried in those numbers are details that could save you money, flag errors, or alert you to problems before they spiral. Here’s how to decode your mortgage statement line by line, and what red flags to watch for.

What Is a Mortgage Statement?

A mortgage statement is a monthly billing notice from your loan servicer detailing your loan activity, current balance, and the breakdown of your upcoming payment. Since 2014, federal law (under the RESPA mortgage servicing rules) requires most servicers to send a statement for each billing cycle, so you have a legal right to this information.

Key Sections of Your Mortgage Statement

1. Account and Loan Information

At the top, you’ll typically find your loan number, property address, servicer contact information, and your current interest rate (if you have an adjustable-rate mortgage, this matters a lot). Verify these basics first — errors here, while rare, do happen.

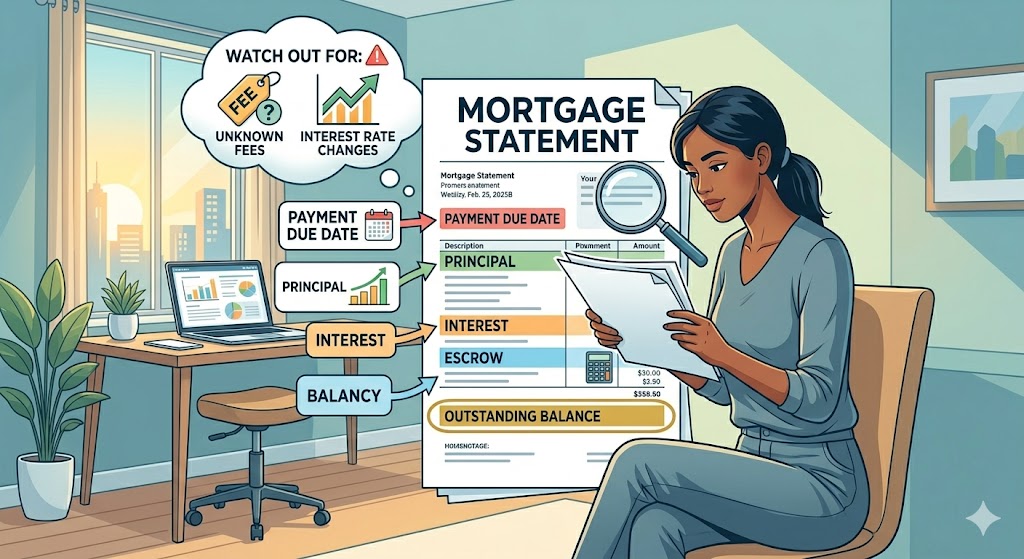

2. Payment Due Date and Amount

This section shows exactly how much is due and when. Look for any late fee notice or past-due amount listed separately. If you see a “payment due” that seems higher than usual, don’t assume it’s correct — read further.

3. Payment Breakdown (Principal, Interest, Escrow)

This is the heart of your statement. Your monthly payment is typically split into three parts:

- Principal – The portion that actually reduces your loan balance.

- Interest – The cost of borrowing. Early in your loan, this takes up the largest share.

- Escrow – Funds collected to pay your property taxes and homeowner’s insurance on your behalf.

In the early years of a 30-year mortgage, it’s normal for interest to dwarf the principal payment. Over time, that ratio flips — which is why making extra principal payments early in your loan saves the most money.

4. Current Loan Balance

This is your outstanding principal — what you still owe. Note that this figure does not reflect any interest that has accrued since your last payment. If you’re considering paying off your loan early, request a payoff quote separately, which will include all fees and accrued interest.

5. Escrow Account Summary

If your lender collects escrow, this section shows what’s held in your escrow account and how it’s projected to be used. Servicers are required to keep only a small cushion above your actual obligations — no more than two months’ worth of payments. If your escrow balance seems unusually high, you may be owed a refund.

6. Transaction History

A record of recent payments, showing how each was applied. Check this every few months to confirm your extra principal payments (if you make them) are being applied correctly — not just held as a future payment.

What to Watch Out For

Escrow shortages. When property taxes or insurance premiums rise, your servicer recalculates your escrow. You may suddenly owe a shortage payment and face a higher monthly bill. Review the annual escrow analysis statement carefully to understand why.

Misapplied payments. If you send extra money, confirm in the transaction history that it went to principal. Some servicers apply it to future payments instead unless you specifically direct otherwise in writing.

Force-placed insurance. If your homeowner’s policy lapses, your servicer can purchase insurance on your behalf — often at a dramatically higher cost — and charge it to your account. Watch for unexpected escrow increases or line-item charges you don’t recognize.

Adjustable-rate changes. If you have an ARM, your statement should show your current rate and any upcoming adjustment. Know your rate caps and adjustment dates so you’re never surprised.

Suspicious fees. Late fees, processing charges, or “property inspection fees” should all be questioned. Servicers are prohibited from collecting fees not authorized by your loan agreement.

The Bottom Line

Your mortgage statement is more than a bill — it’s a financial report on one of your largest assets. Taking ten minutes each month to review it can catch errors, prevent surprises, and keep you firmly in control of your path to ownership.