Life insurance is a financial product that provides monetary support to beneficiaries when the insured individual passes away. This product is crucial for families as it ensures financial stability and security during challenging times. By choosing the appropriate life insurance policy, families can mitigate the financial burden caused by the loss of a primary income earner or any family member who contributes financially.

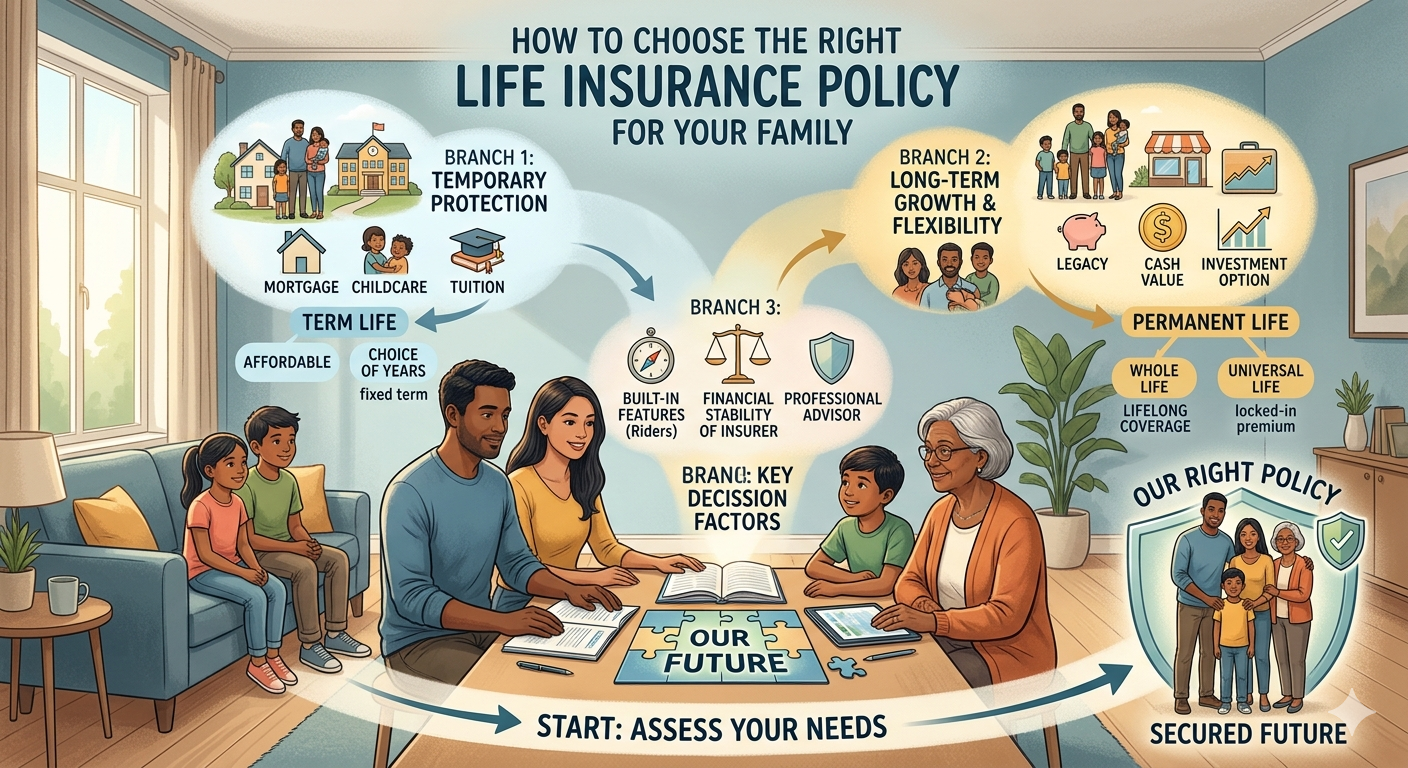

There are three primary types of life insurance policies available: term life, whole life, and universal life. Term life insurance is designed to provide coverage for a specified time, usually ranging from 10 to 30 years. During this period, if the policyholder passes away, the designated beneficiaries receive a death benefit. This type of policy is typically more affordable and straightforward, making it an excellent option for families seeking temporary coverage.

In contrast, whole life insurance offers lifelong protection as long as premiums are paid. This policy not only provides a death benefit but also accumulates a cash value over time, which can be accessed during the policyholder’s lifetime. Consequently, whole life insurance serves a dual purpose: it acts as a safety net for loved ones after an individual’s death while also functioning as an investment vehicle.

Universal life insurance offers more flexibility compared to whole life policies. It allows policyholders to adjust premium payments and death benefits, adapting to their financial situation over time. This adaptability can be particularly beneficial for families with changing needs. Understanding essential terms such as beneficiaries, the individuals who will receive the death benefit, premiums, the amount paid for the policy, and death benefits, the sum paid to beneficiaries, is crucial when evaluating different life insurance options.

Assessing Your Family’s Needs

Choosing the right life insurance policy requires a thorough assessment of your family’s specific financial needs and future aspirations. To begin, evaluate your current income. Determining how much your family relies on your earnings will help in deciding the amount of coverage necessary. A policy should ideally provide a safety net that can replace lost income, allowing your family to maintain their standard of living without unexpected financial burdens.

Next, it is essential to consider any existing debts such as a mortgage, credit card balances, or personal loans. Life insurance can serve not only as a financial cushion for your loved ones but also as a means to cover outstanding debts, preventing them from becoming a burden during a challenging time. Calculating the total amount owed will provide a clearer picture of the coverage needed to ensure these liabilities are settled.

Living expenses represent another critical component when assessing your family’s financial landscape. This includes everyday costs such as housing, utilities, groceries, and healthcare. Analyzing your household’s monthly expenses can help you figure out how much life insurance is required to support your family for a given period after your passing.

Moreover, if you have children, contemplate their educational needs. Education costs can escalate significantly, making it imperative to factor in tuition for both primary and secondary schools, as well as higher education. If your family is preparing for potential special considerations, such as caring for a disabled dependent or financing elder care, including these factors will help in tailoring your life insurance policy.

In essence, understanding your family’s comprehensive financial situation and future needs will guide you in selecting the appropriate life insurance policy, ensuring that you provide adequate protection for your loved ones.

Types of Life Insurance Policies Explained

When considering life insurance policies, it is essential to understand the differences between the primary types available: term life insurance, whole life insurance, and universal life insurance. Each of these policies offers unique features and benefits that cater to varying financial needs and goals.

Term life insurance is typically the most affordable option, providing coverage for a specified time, commonly ranging from 10 to 30 years. This type of policy pays a death benefit to beneficiaries only if the insured individual passes away within the designated term. The primary advantage of term life insurance is its low premium cost compared to permanent policies, making it an attractive choice for young families or individuals looking for budget-friendly protection. However, once the term expires, the policyholder must either renew the policy at potentially higher rates or seek new insurance coverage, which can be more costly due to age or health changes.

In contrast, whole life insurance offers lifelong protection, as it does not expire as long as premiums are paid. This policy also accumulates cash value over time, which can be borrowed against or withdrawn. Whole life insurance tends to have higher premiums, reflecting its lifelong coverage and cash value feature. Families seeking a long-term financial foundation that includes a savings component may find whole life insurance to be a suitable choice.

Universal life insurance introduces flexibility, allowing policyholders to adjust their premiums and death benefits as their financial situations change. Like whole life insurance, it builds cash value, but it typically offers more investment options. This adaptability can be beneficial for families whose needs may evolve over time. Understanding these distinctions is crucial when choosing the right policy to ensure comprehensive coverage for one’s family.

Choosing the Right Coverage Amount

Determining the appropriate coverage amount for a life insurance policy is crucial in providing financial security for one’s family in the event of an unforeseen tragedy. Various methods can assist individuals in calculating the necessary coverage, with the income replacement approach being one of the most common strategies. This method considers the insured’s income and estimates how much money the family would require to maintain their current lifestyle without the deceased’s financial contribution. Typically, a multiple of the yearly income is chosen, often ranging from 5 to 15 times the annual salary, to derive a suitable coverage amount.

Another approach is the financial obligations method, which focuses on assessing an individual’s current debts and future obligations. This includes not just existing home loans, car loans, and credit card debts, but also any anticipated expenses such as college tuition for children and retirement savings. By summing these financial responsibilities, one can arrive at an adequate coverage figure that aims to eliminate financial burdens on the family.

The needs analysis method adds a layer of personalization to the calculation by evaluating specific needs and objectives of the family. This comprehensive approach requires detailing immediate needs such as funeral expenses, mortgage balances, and ongoing living expenses, alongside long-term goals like children’s education funds and retirement planning. This nuanced analysis ensures that no aspect of the family’s financial future is overlooked.

It is vital to review life insurance coverage periodically, as personal circumstances change over time. Significant life events such as marriage, the birth of children, or changes in income may necessitate a reassessment of coverage levels. Regularly evaluating these factors ensures that the policy continues to meet evolving family needs effectively.

Evaluating Insurance Providers

When selecting a life insurance policy for your family, it is crucial to evaluate various insurance providers meticulously. This evaluation process involves several factors that will help ensure you choose a reliable company that meets your needs.

First and foremost, assess the reputation of the insurance provider. This can be done by examining reviews and ratings from reputable sources. Online customer reviews offer insights into real experiences, providing a clearer picture of the company’s trustworthiness. Additionally, organizations such as the Better Business Bureau provide accreditation ratings that reflect a company’s commitment to resolving customer complaints and maintaining positive relationships.

Financial stability is another critical factor. A life insurance company’s financial health can be gauged through ratings from agencies like A.M. Best, Moody’s, or Standard & Poor’s. These ratings express the insurer’s ability to meet its future policyholder obligations, indicating whether a provider will be capable of paying out claims when necessary. A provider rated ‘A’ or above generally suggests strong financial stability.

Another important aspect to consider is customer service. Efficient customer service is paramount for any insurance provider, particularly when a claim needs to be processed. Access to resources such as a dedicated claims hotline or online chat support can significantly enhance the customer experience. A company’s responsiveness and ability to provide clear, timely information will also influence your overall satisfaction.

Finally, take the time to analyze the range of policy options available, including flexibility. A good life insurance provider should offer various policy types—such as term, whole, or universal life insurance—allowing you to tailor coverage to your family’s unique needs. It’s essential to choose a plan that provides the necessary coverage while allowing for future adjustments as family circumstances change.

Understanding Policy Terms and Conditions

When considering a life insurance policy, it is essential to thoroughly understand the policy terms and conditions detailed in the document. Reading the fine print is not merely a recommendation; it is a necessity to avoid potential pitfalls that could affect your family’s financial security. Policies often contain various terms that may not be immediately clear, such as coverage limits, exclusions, riders, and contingencies that can significantly influence the benefits provided under the policy.

One common area of confusion arises from exclusions stated within the policy. These exclusions outline specific circumstances or events for which the insurer will not pay benefits. For example, certain policies may exclude death resulting from suicide within a specified period after the policy is purchased. Understanding these exclusions can help you assess whether the policy provides sufficient coverage in scenarios that may affect your family.

Additionally, riders can offer supplementary benefits or modify the standard policy terms, giving you the flexibility to tailor the coverage to fit your unique needs. Riders could include options for accidental death or critical illness coverage, but it’s crucial to review the costs associated with these add-ons and how they may affect the overall premiums. Individuals should not hesitate to ask for clarifying information regarding these riders or how they interact with the primary coverage.

Changes in terms over time can also be a significant concern. Insurers may revise the terms and conditions of the policy, including premium rates and benefit limits. It is advisable to inquire about the possibility of changes and how they might impact your current coverage. Always request clarification from your insurance provider to ensure you fully comprehend every aspect of the policy before making your purchase.

The Importance of Shopping Around

Choosing the right life insurance policy for your family is a crucial decision that requires thorough evaluation and comparison. One of the most effective ways to ensure that you secure the best coverage for your needs at a competitive price is by shopping around. By receiving multiple quotes from various insurance providers, you gain a comprehensive view of the market, allowing you to make an informed decision tailored to your family’s unique requirements.

When comparing quotes, it is essential to utilize a variety of tools and resources. Numerous online platforms allow consumers to compare life insurance policies side-by-side, providing a snapshot of coverage options, premiums, and benefits. These tools not only save time but also facilitate an understanding of different policies, ensuring no vital details are overlooked.

Additionally, engaging with an insurance agent or broker can further streamline the process. These professionals possess intricate knowledge of the life insurance landscape and can help interpret technical terminology, making it easier for you to understand the nuances between policies. They can also offer personalized recommendations based on your financial situation and long-term goals. While leveraging their expertise may involve a service fee or commission, it is often worthwhile for consumers who seek clarity and reassurance in navigating the complexities of life insurance.

Ultimately, the significance of shopping around cannot be overstated. By diligently comparing various life insurance options, understanding the roles of agents and brokers, and utilizing available resources, you increase your chances of finding a policy that provides adequate financial protection for your family. Taking the time to perform such due diligence will not only ensure that you are making a sound investment in your family’s future but also help optimize the benefits of the life insurance policy you ultimately choose.

Reviewing and Adjusting Your Policy Over Time

Life insurance is not a one-time decision; it is essential to regularly review and adjust your policy to ensure it continues to meet your family’s needs. Over time, various factors can significantly influence the adequacy of your coverage, including major life events and changes in your financial situation. By keeping your policy aligned with your current circumstances, you can maintain peace of mind.

One prominent reason for a policy review is major life events. For instance, marriage is a significant milestone that often warrants an reevaluation of your life insurance coverage. With a partner to support, you may wish to increase your policy to ensure financial protection for your spouse. Similarly, the birth of a child is another critical turning point that typically necessitates an overhaul of your life insurance policy, as you’ll want to secure your child’s future. Additionally, job changes or promotions that increase your income may require adjustments to your coverage to reflect your new financial responsibilities.

Another critical factor to consider is the evolution of your financial goals. As you progress through different life stages, your financial objectives may shift dramatically; this could involve paying off a mortgage, funding a child’s education, or preparing for retirement. Your life insurance policy should adapt alongside these goals. If your financial status improves, you might choose to enhance your coverage, thereby providing additional financial security for your loved ones. Conversely, if financial challenges arise, it may be necessary to reevaluate your policy to ensure it remains affordable while still offering adequate protection.

In essence, a proactive approach to reviewing and adjusting your life insurance policy fosters financial security for your family. Regular assessments empower you to align your coverage with your evolving life circumstances, ultimately ensuring that you provide the necessary support for your loved ones in their time of need.

Conclusion and Next Steps

As we have discussed throughout this article, selecting the appropriate life insurance policy is critical for securing your family’s financial future. Life insurance serves as a safety net that provides financial support to your loved ones in the event of an unforeseen circumstance. Understanding the different types of policies available, along with your family’s specific needs, is vital in making a well-informed decision.

The importance of evaluating your financial situation cannot be overstated. Assessing factors such as total income, debts, and future expenses—like your children’s education—will enable you to determine the amount of coverage that is appropriate for your household. Moreover, it’s essential to familiarize yourself with the various life insurance products offered, including term life, whole life, and universal life insurance, to find the best fit for your unique circumstances.

Next steps involve taking actionable measures towards securing a suitable policy. Firstly, consider consulting a professional financial advisor or insurance agent who can provide personalized guidance based on your family’s goals. They can help clarify the intricacies of different life insurance options and assist in tailoring a policy that aligns with your needs.

Additionally, conducting online research can prove beneficial. Many websites offer quotes and comparisons which allow you to analyze different policies without commitment. This will not only give you a clearer picture of available options but will also empower you to make a more educated decision.

Lastly, once you feel confident about your choice, initiate the application process. Ensure that all information provided during the application is accurate to avoid complications in the future. With these steps, you can secure peace of mind knowing that your family’s financial security is well protected.