Mortgage refinance rates represent the interest rates charged on new mortgage loans taken to replace existing ones. This process, commonly referred to as refinancing, allows homeowners to adjust their mortgage terms, potentially lowering monthly payments or accessing equity in their property. The rates offered to borrowers can vary significantly based on a variety of factors, including credit score, loan-to-value ratio, and current market conditions.

Several types of mortgage refinancing options are available, each tailored to meet specific borrower needs. Rate-and-term refinancing is the most common type, where the existing loan is refinanced to secure a lower interest rate or modify the loan term. This approach can result in substantial savings on monthly payments, making homeownership more affordable over time.

On the other hand, cash-out refinancing allows homeowners to refinance more than what is owed on the existing mortgage, receiving the difference in cash. This option can be beneficial for those seeking funds for home improvements, debt consolidation, or other expenses. However, it is crucial for borrowers to weigh the potential risks, such as increased debt and the possibility of foreclosure should they fail to keep up with payments.

The mortgage refinance rate a borrower can secure is influenced by numerous factors. A strong credit score generally translates into better rates, as lenders view borrowers with higher scores as less risky. Additionally, the overall economic climate, including the Federal Reserve’s monetary policy and prevailing budgetary practices, can cause rates to fluctuate. Thus, staying informed about market trends and maintaining good credit health is vital for anyone considering mortgage refinancing.

Current Trends in Mortgage Refinance Rates

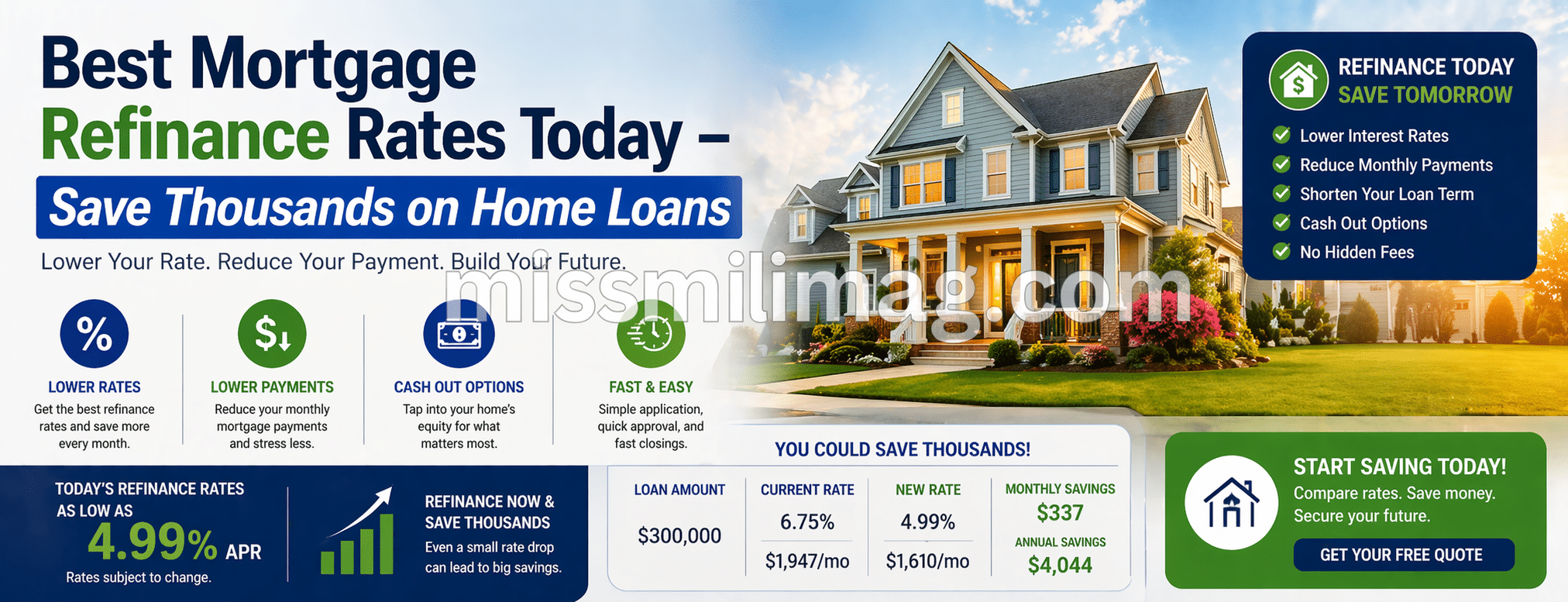

As of today, the landscape for mortgage refinance rates remains dynamic, reflecting various economic factors and market conditions. Currently, mortgage refinance rates generally hover in a range of 6% to 7.5%, depending on individual circumstances such as credit scores, loan amounts, and geographic locations. This range marks a notable increase compared to the historically low rates observed during the pandemic years, which sometimes dipped below 3%.

To provide a clearer perspective, according to data from the Mortgage Bankers Association, the average refinance rate for a 30-year fixed mortgage was around 6.5% in October 2023. This is significantly higher than the rates recorded last year, prompting homeowners to reconsider the timing of refinancing their current loans. It is essential to recognize that economic influences, particularly changes in federal policies, drive these fluctuations. The Federal Reserve’s decision to implement interest rate hikes in response to inflation has contributed to rising mortgage refinance rates.

Additionally, it is observed that while rising rates may discourage immediate refinancing for some homeowners, others can still find substantial savings opportunities. Homeowners with existing higher-rate mortgages from previous years may benefit from refinancing at a lower rate if they qualify. Forward-looking indications suggest that mortgage refinance rates might stabilize in the near future, provided inflationary pressures begin to taper off and if the Fed pauses further rate hikes. Keeping track of these trends can empower homeowners to make informed decisions regarding their mortgage options.

How to Secure the Best Mortgage Refinance Rates

Securing the best mortgage refinance rates is a strategic process that requires careful planning and consideration. One of the most critical factors influencing refinance rates is the credit score. Homeowners should actively work on improving their credit scores before applying for refinancing. This can involve paying down debts, ensuring timely bill payments, and checking credit reports for inaccuracies. A higher credit score can significantly lower the interest rate offered, thus leading to potential savings over the life of the loan.

The timing of refinancing is another essential consideration. Interest rates fluctuate based on various economic factors, and homeowners should keep an eye on market trends. Consulting with a financial advisor or utilizing online mortgage calculators can provide insights into the optimal time to refinance. Generally, if the current mortgage rate is at least 1% lower than the existing rate, it may be beneficial to consider refinancing.

Shopping around for mortgage refinance rates is vital to finding the best deal. Homeowners should obtain quotes from multiple lenders, including banks, credit unions, and online mortgage companies. Comparing rates and terms can help identify options that align with personal financial goals. Additionally, it is important to consider points and fees associated with refinancing. Homeowners may choose to pay points upfront to secure a lower interest rate. However, the decision to pay points should be weighed against the expected time spent in the home and the overall financial advantages that could be gained from these lower rates.

By focusing on credit score management, timely refinancing, diligent shopping for rates, and careful consideration of associated costs, homeowners can secure favorable mortgage refinance rates and potentially save thousands over the term of their mortgage.

Potential Savings and Considerations for Refinancing

Refinancing a mortgage presents homeowners with the opportunity to save considerably on their home loans. The primary reason for refinancing is to secure a lower interest rate, which can reduce monthly payments and decrease the overall amount paid over the life of the loan. For instance, if a homeowner refinances from a 4.5% interest rate to a 3.0% rate, they can save thousands in interest payments, particularly over a long-term loan of 30 years.

Another common scenario occurs when homeowners wish to switch from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage, providing predictability in payments over time. Moreover, refinancing can also enable homeowners to tap into equity for significant expenses, such as home improvements or debt consolidation, which might lead to further financial relief.

However, it is essential to weigh the costs associated with refinancing against the savings expected. Closing costs, which can range from 2% to 5% of the loan amount, must be factored into any calculation of the benefits. Homeowners should also consider the duration they plan to stay in their home; refinancing only makes sense if the new monthly savings exceed the closing costs within a reasonable timeframe.

Additionally, potential pitfalls such as prepayment penalties on existing loans or taking on a longer repayment term can negate the intended benefits of refinancing. A thorough cost-benefit analysis is crucial before making any decisions. Homeowners are advised to compare multiple mortgage refinance rates to ensure that they secure the best possible deal while keeping these considerations in mind.