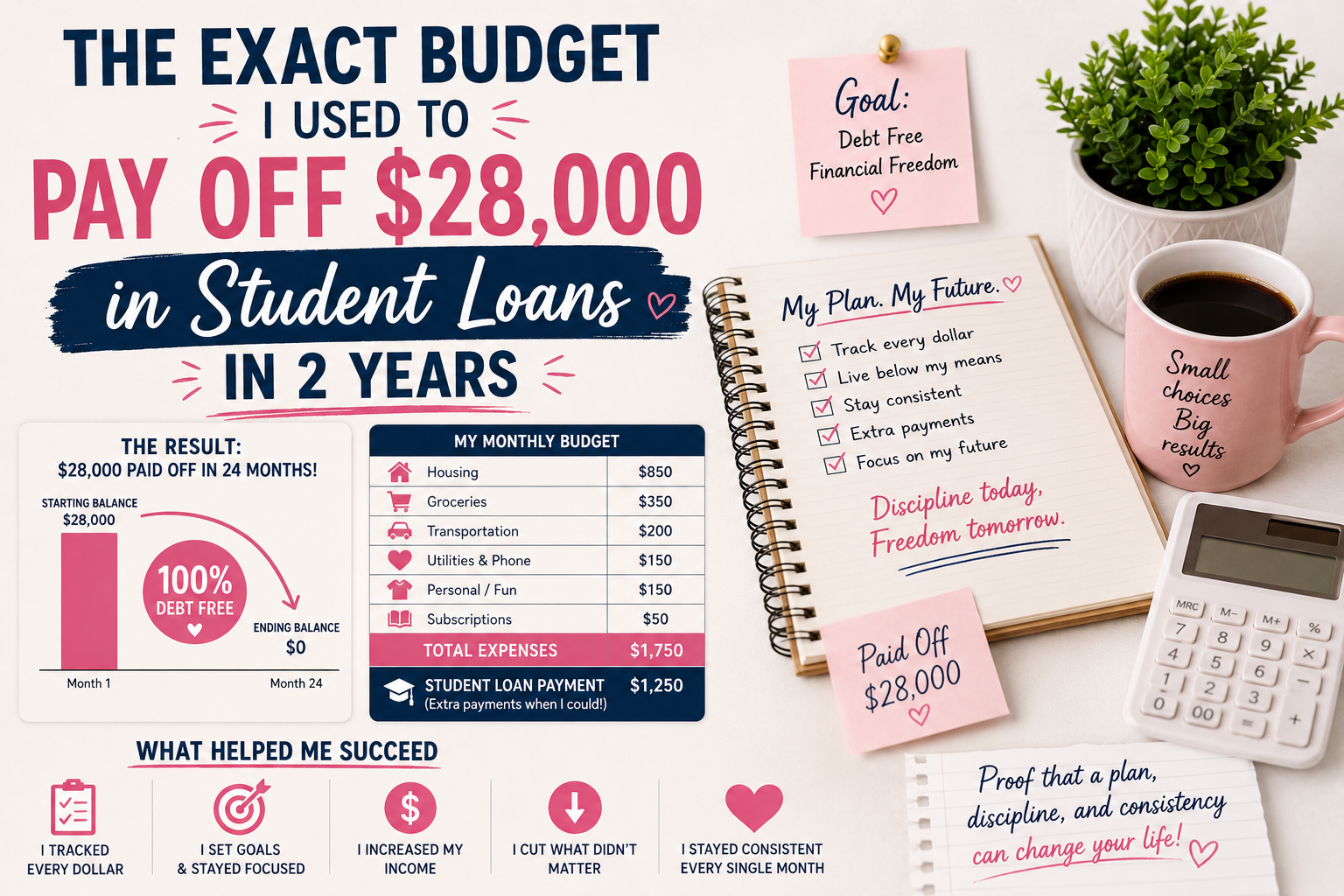

The air in my tiny studio apartment felt heavy the night I finally faced the numbers. Sitting on a secondhand rug, glowing under the harsh light of a laptop screen, I stared at a number that made my stomach drop: $28,432.

Fresh out of college, that student loan balance felt less like a financial milestone and more like a permanent anchor. With an entry-level take-home salary of $4,000 a month, paying it off felt generations away. Yet, exactly 24 months later, I made my final payment.

I didn’t win the lottery, and I didn’t have a secret trust fund. What I had was a hyper-focused, radical budgeting strategy. If you are drowning in debt and looking for a realistic financial roadmap, this is the exact budget breakdown I used to crush $28,000 in student loans in just two years.

The Wake-Up Call: Facing the “Before” Budget

Before finding my financial footing, my money just sort of… evaporated. I was practicing “scarcity budgeting”—checking my banking app at the grocery checkout line, hoping my card wouldn’t get declined.

To pay off $28,000 in 24 months, the math was unyielding. I needed to put roughly $1,200 every single month toward my principal and interest. On my $4,000 monthly income, that meant 30% of my paycheck had to disappear into the debt abyss immediately. I had to slice my living expenses down to the absolute bone.

The Exact Monthly Blueprint

To make it work, I adopted a heavily modified version of the traditional 50/30/20 budget. Instead of saving 20% or using it for fun, my breakdown looked like an aggressive 50/20/30 split: 50% for fixed needs, 20% for flexible lifestyle choices, and a massive 30% strictly funneled into my student loans.

Here is exactly how my $4,000 monthly take-home income was distributed each month:

-

The Debt Avalanche: I dedicated a flat $1,200 (30%) directly to my student loans.

-

Rent & Utilities: By splitting a place with a roommate, I kept my housing costs at $1,100 (27.5%).

-

Groceries & Basic Sustenance: I kept meal planning strict, spending $350 (8.75%) on food.

-

Transportation: Between a public transit pass and basic insurance for my old car, this took $250 (6.25%).

-

Emergency Fund: I maintained a tiny savings buffer of $300 (7.5%) for unexpected emergencies.

-

The “Keep Me Sane” Fund: The remaining $800 (20%) went to everything else—dining out, streaming subscriptions, and general life.

The Two Rules That Saved My Sanity

Living on this budget wasn’t a walk in the park. It required structural lifestyle shifts that kept me on track month after month.

1. The “Pre-Game” Payment Method

I never gave myself the chance to spend my debt money. The day my paycheck hit my account, $600 (half of my monthly goal) was automatically transferred directly to my loan servicer. If I didn’t see it in my checking account, I couldn’t mistake it for spending money.

2. The Micro-Hustle Pivot

Let’s be honest: an $800 flexible spending budget gets eaten up incredibly fast by unexpected car repairs or a friend’s birthday dinner. Whenever my lifestyle budget took a hit, I refused to lower my $1,200 loan payment. Instead, I picked up weekend pet-sitting gigs and sold old clothes online. Every single dollar from those side hustles went straight to the loans.

The Finish Line

That final month, typing in a payment of $1,142 and seeing the balance update to $0.00 was indescribable. The heavy air in my apartment completely cleared.

Paying off $28,000 in two years didn’t require algorithmic genius; it required consistency and a willingness to live a little smaller for a short time so I could live much larger later. If you are staring down your own mountain of debt today, block out the noise. Grab a spreadsheet, find your numbers, and remember that every sacrifice you make today is a direct investment in your future freedom.