Hitting your 30s is a major financial pivot point. By now, you are likely hitting your stride in your career, watching your income grow, and starting to look seriously at the horizon. If you are a millennial or Gen Z woman in this decade, saving for the future is no longer a “someday” task—it is a “right now” priority.

When looking at individual retirement accounts (IRAs), you will face a critical forks-in-the-road choice: Roth IRA vs. Traditional IRA. Both are powerful wealth-building tools, but they handle taxes in completely opposite ways.

Choosing the right container for your money depends on your current career path, income trajectory, and long-term goals.

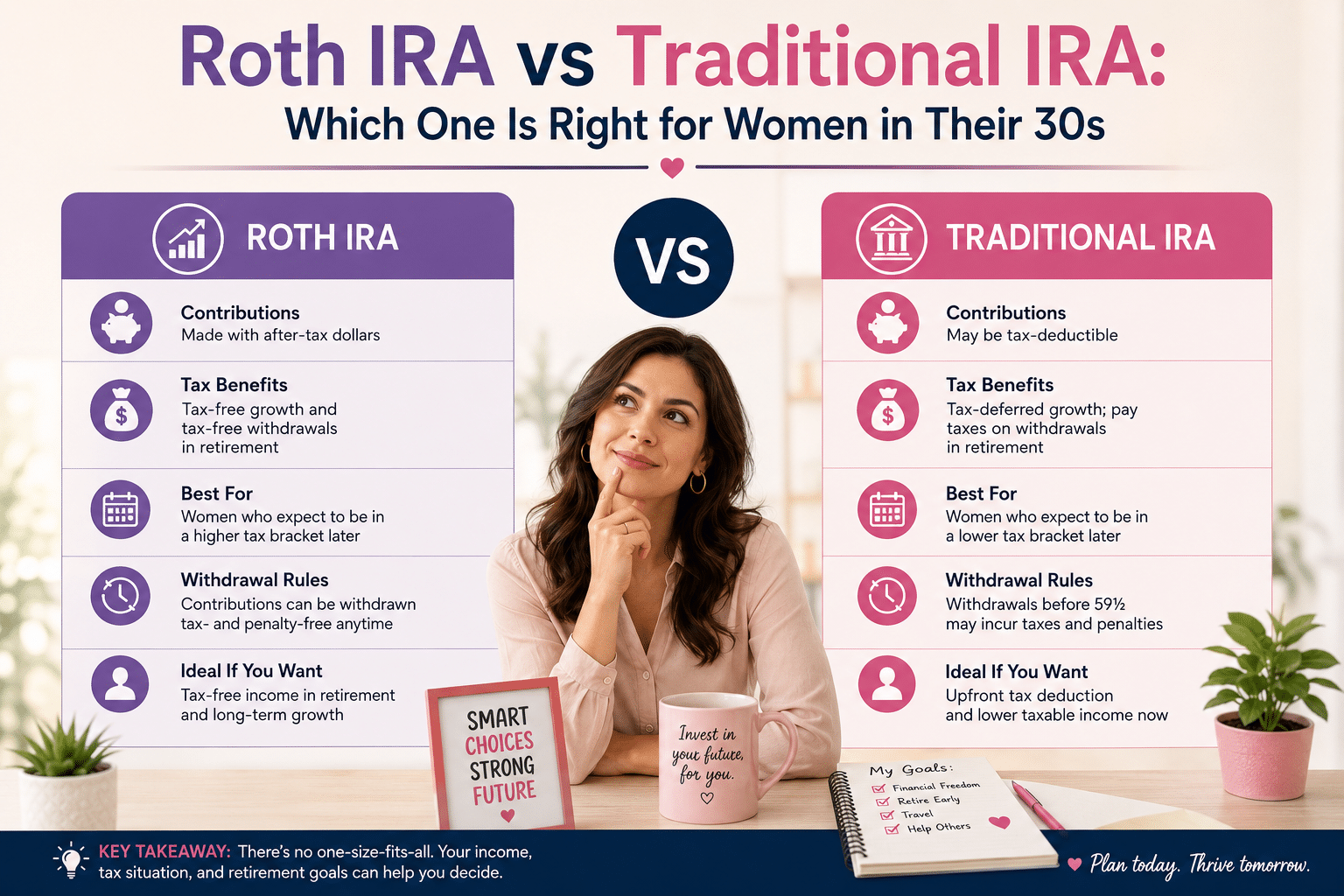

The Core Difference: Pay Taxes Now or Later?

The easiest way to understand the difference between these two accounts is to look at when Uncle Sam takes his cut.

-

Traditional IRA: You get a tax break today. Your contributions can often be deducted from your current taxable income, meaning you pay less in taxes this year. However, when you withdraw the money in retirement, both your original contributions and the investment growth are taxed as regular income.

-

Roth IRA: You get a tax break later. You invest “after-tax” dollars—meaning you get no upfront tax deduction. The massive payoff happens down the road: your investments grow completely tax-free, and your withdrawals in retirement are 100% tax-free.

Why Your 30s Are the Golden Window for a Roth IRA

For many women in their 30s, the Roth IRA emerges as the clear winner. Here is why this decade provides the perfect environment for a Roth account to thrive:

1. You Likely Haven’t Hit Your Peak Earnings Yet

In your 30s, you might be making good money, but your earning potential will likely climb even higher in your 40s and 50s. If you expect to be in a higher tax bracket later in life (or during retirement) than you are right now, paying taxes today at your current lower rate via a Roth IRA is a massive win.

2. Decades of Compounding Left

Time is an investor’s greatest asset. If you are in your 30s, your money has roughly 30 years to compound before you touch it. Because a Roth IRA allows your investment growth to build completely untaxed, the compound interest snowball becomes incredibly powerful. You are essentially letting decades of stock market growth accumulate entirely free of tax liabilities.

3. Ultimate Flexibility for Major Life Events

Women often face unique career interruptions, whether for caregiving, starting a business, or expanding a family. One unique feature of the Roth IRA is its flexibility: you can withdraw your original contributions at any time, for any reason, with zero taxes or penalties. While you should leave your retirement money alone if possible, knowing you can access that baseline capital provides an excellent secondary safety net.

When a Traditional IRA Makes More Sense

While the Roth IRA gets a lot of love, a Traditional IRA is a stellar choice under specific circumstances:

You Are Already a High Earner

If your career has taken off and you find yourself in a high tax bracket today, you might want immediate tax relief. A Traditional IRA can lower your Adjusted Gross Income (AGI) right now, keeping more money in your pocket during tax season.

You Lower Your Taxable Income with Business Deductions

If you are a freelancer or business owner in your 30s, utilizing a Traditional IRA can be a strategic move to aggressively manage your annual tax liability alongside other business write-offs.

The Guardrails: Contribution and Income Limits

No matter which account you choose, the IRS sets strict boundaries on who can participate and how much you can tuck away.

For the 2026 tax year, the combined maximum amount you can contribute to all your traditional and Roth IRAs is $7,500 (for anyone under age 50).

-

Roth Income Limits (2026): To make a full contribution to a Roth IRA, your Modified Adjusted Gross Income (MAGI) must be under $153,000 if you file as single, or under $242,000 if you are married filing jointly.

-

Traditional Deduction Limits (2026): Anyone with earned income can contribute to a Traditional IRA, but your ability to deduct those contributions on your taxes phases out if you have access to a retirement plan at work (like a 401k) and your income exceeds certain thresholds ($81,000 for single filers).

The Verdict: Which One Should You Choose?

If you are a woman in your 30s making an average to upper-average income, lean toward the Roth IRA. The promise of tax-free growth and tax-free retirement income is incredibly hard to beat, especially when you have decades of market compounding ahead of you.

However, if you are focused on slashing a high tax bill today, a Traditional IRA will give you that instant gratification. Whichever path you choose, the most important step is simply getting your money into the market so it can start working for you.