Life insurance is a financial product that provides a safety net for individuals and their loved ones in the event of an unexpected death. It works by the insured paying regular premiums in exchange for a lump sum payment, known as a death benefit, to the beneficiaries upon the policyholder’s passing. While traditionally associated with individuals in their older years or those with families, life insurance is increasingly becoming a vital component of financial planning for young adults.

There are various types of life insurance policies available, including term life and whole life insurance. Term life insurance provides coverage for a specified period, typically between 10 to 30 years, while whole life insurance covers the insured for their entire life and usually accumulates cash value over time. Understanding these options can help young adults choose a policy that best aligns with their financial goals and lifestyle.

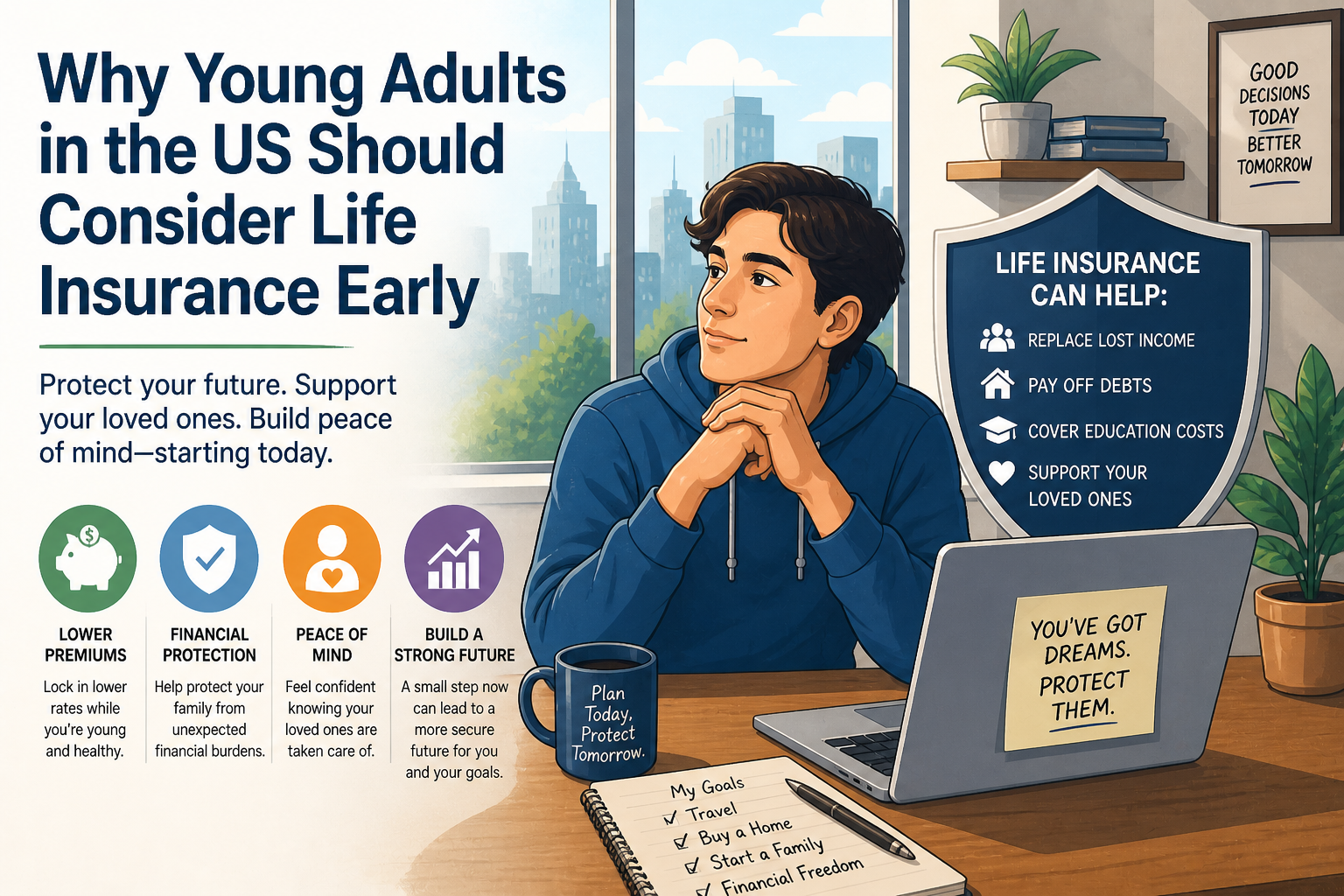

Many young adults harbor misconceptions about life insurance, believing it to be unnecessary or overly expensive at their stage in life. However, not only does acquiring life insurance at a young age often result in lower premiums, but it also ensures that individuals are covered in the event of unforeseen circumstances. Furthermore, young adults may have financial obligations, such as student loans, which could burden their family in the case of their untimely demise. By securing life insurance early, they can alleviate this potential financial strain.

In a world where financial responsibilities can arise unexpectedly, it is crucial for young adults to prioritize financial planning. Life insurance should be considered not merely as a precautionary measure, but as a proactive step toward safeguarding one’s financial future. Taking action today can lead to a more secure tomorrow, encouraging young adults to view life insurance as an essential part of their overall financial strategy.

The Importance of Financial Security

Financial security is a crucial aspect of young adulthood that often goes overlooked. Many young adults are in the early stages of their careers and may not fully appreciate the importance of safeguarding their financial future. Life insurance serves as a vital tool to help mitigate potential risks and ensure that both individuals and their dependents remain protected against unforeseen circumstances.

One of the primary functions of life insurance is to provide a safety net for dependents. Young adults who have children or other individuals who rely on them financially should consider how the absence of their income would impact those loved ones. A life insurance policy can alleviate this burden by offering financial support in the event of an untimely death, thereby allowing dependents to maintain their standard of living and cover essential expenses such as housing, education, and healthcare.

Additionally, life insurance can play a significant role in reducing financial burdens associated with outstanding debts. Many young adults may carry student loans, credit card debt, or personal loans. In the case of an unexpected tragedy, these debts do not simply vanish; they can become the responsibility of surviving family members. By having life insurance in place, young adults can ensure that their debts are settled without placing an additional financial strain on their loved ones.

Moreover, being unprepared for unforeseen circumstances can lead to long-term financial ramifications. Without proper planning, young adults risk leaving their families in dire situations, struggling with financial instability. By taking proactive measures to secure life insurance early on, they can foster peace of mind, knowing they have laid a foundation of financial security for their dependents. Consideration of life insurance is not merely an act of financial prudence; it is an essential step towards protecting against the unexpected.

Affordability of Life Insurance for Young Adults

Life insurance is often viewed as an unnecessary expense by many young adults in the United States; however, the truth is that it can be quite affordable. In fact, younger individuals typically qualify for lower premiums compared to older adults. This cost advantage arises from several factors, including better health prospects, lower risk of mortality, and the potential for longer-term savings. The life insurance industry often relies on age and health status to determine policy rates, and as a result, young adults are generally considered to be in lower-risk categories.

There are two main types of life insurance commonly available: term life insurance and whole life insurance. Term life insurance is typically the more budget-friendly option, offering coverage for a specific period, typically ranging from 10 to 30 years, at a lower cost. This makes it particularly appealing for young adults who may have tighter budgets while needing ample coverage for dependents or debts, such as student loans. Moreover, the premiums remain level throughout the term, allowing for predictable costs.

On the other hand, whole life insurance can be more expensive, as it not only provides lifelong coverage but also includes an investment component. However, investing in whole life insurance at a young age can result in significant long-term savings, due to lower initial premiums and the cash value growth over time. This aspect makes it a viable option for health-conscious young adults looking for both coverage and an investment opportunity.

Ultimately, the affordability of life insurance for young adults makes it a prudent financial decision. By investing early, individuals can lock in lower rates, ensuring financial protection for themselves and their families while potentially saving substantial amounts over the lifetime of the policy.

Types of Life Insurance Available

When considering life insurance, young adults in the US have several options to choose from. The three primary types of life insurance policies are term life insurance, whole life insurance, and universal life insurance. Each type has distinct features, benefits, and limitations that can impact the decision-making process.

Term life insurance provides coverage for a specified period, typically ranging from 10 to 30 years. This type is often favored for its affordability, as premiums tend to be lower compared to whole life insurance. The benefits of term life insurance include its straightforward nature and the ability to provide substantial coverage for a relatively low cost. However, once the term expires, the policyholder has no coverage unless they renew or convert it to a permanent policy, which may come at a higher premium.

Whole life insurance offers lifelong coverage and includes a cash value component that grows over time. This type of insurance is generally more expensive than term insurance, but it provides guaranteed death benefits and can serve as a financial asset that can be borrowed against. The predictability of premiums and the growth of cash value make whole life insurance an attractive option for some. Nonetheless, the higher costs and potential complexities associated with this type might be off-putting for young adults just beginning their financial journey.

Universal life insurance combines flexibility with the benefits of permanent coverage. Policyholders can adjust their premiums and death benefits, allowing for responsiveness to changing financial circumstances. Additionally, universal life insurance builds cash value, though the growth is subject to market performance, which may result in less predictability compared to whole life insurance. While this type may appeal to those seeking customization, it often requires more engagement to ensure the policy remains effective over time.

Real-Life Scenarios and Testimonials

The importance of life insurance cannot be overstated, especially for young adults in the United States. Numerous individuals have shared their stories emphasizing how acquiring life insurance at an early age profoundly impacted their lives and those of their loved ones. For instance, Sarah, a 28-year-old nurse, decided to purchase a life insurance policy shortly after obtaining her first job. She recognized the significance of safeguarding her family’s financial future. When her mother fell ill unexpectedly, the financial burden of medical expenses became overwhelming. However, Sarah found solace in knowing that her life insurance would cover additional costs incurred during this challenging time.

Another testimonial comes from Ethan, a 25-year-old entrepreneur, who invested in a life insurance policy to secure funds for his future family. Ethan recalled, “I used to think life insurance was a luxury. However, when I started my business, I understood how unpredictable life can be. Having life insurance at my age gave me the peace of mind to take risks without worrying about what might happen to my loved ones. If anything were to happen to me, I know they would be taken care of.” His proactive approach highlights how early life insurance planning can serve as a safety net, providing both financial security and emotional reassurance.

Moreover, a study further supports these testimonials, showing that young adults who invest in life insurance tend to feel a greater sense of security concerning their financial future. This reality is echoed in the experiences of individuals who have benefited from life insurance policies during unforeseen events. These real-life scenarios underline the potential peace of mind that comes from making informed decisions about life insurance at an early age.

How to Choose the Right Life Insurance Policy

Choosing the appropriate life insurance policy is a crucial decision that young adults in the US should make, particularly when considering their financial future and family responsibilities. The first step in this process is to assess your financial needs accurately. This includes determining how much coverage you need based on potential future expenses, such as mortgages, education, and debt repayment. A commonly recommended approach is to multiply your annual income by a factor of ten to estimate the coverage amount, but individual circumstances may vary significantly.

Next, it is important to explore different types of life insurance policies available. The two primary categories are term life insurance and whole life insurance. Term life policies provide coverage for a specified period, usually ranging from 10 to 30 years, while whole life insurance offers lifelong protection and a cash value component. Understanding these differences will help you determine which type aligns better with your financial goals.

Additionally, researching various insurance providers is essential. Look for companies with a strong reputation, solid financial standing, and positive customer reviews. Online comparison tools can facilitate this process by allowing you to evaluate quotes and policy features side by side. Furthermore, consulting with an insurance professional can provide valuable insights tailored to your personal situation. An expert can offer recommendations based on industry knowledge, ensuring that you select a policy that fits your specific requirements.

Lastly, it is prudent to review your life insurance policy regularly, especially as your financial situation evolves over time. Life changes such as marriage, the birth of a child, or significant promotions may necessitate adjustments to your coverage. By periodically reassessing your needs, you ensure that your life insurance policy remains relevant and adequately protects your beneficiaries.

Common Myths and Misunderstandings about Life Insurance

Many young adults in the United States shy away from purchasing life insurance due to prevalent myths and misunderstandings. One of the most common misconceptions is that life insurance is only necessary for older individuals or those with families. On the contrary, even young, single adults can benefit from a life insurance policy. It can act as financial protection for student loans or other debts, ensuring that these burdens do not fall onto family members in the event of an untimely death.

Another widespread myth is the belief that life insurance is prohibitively expensive. While it is true that rates can vary based on numerous factors, young and healthy individuals typically qualify for lower premiums. Some insurance providers offer affordable options specifically designed for young adults, making it financially feasible to secure a policy early on.

A common fear surrounding life insurance is the notion that it is too complicated to understand. In reality, life insurance policies come in various forms, including term life and whole life insurance, each with its benefits and drawbacks. Resources are available online and through financial advisors to clarify any confusing aspects of life insurance, making it easier for individuals to choose the right coverage for their needs.

Furthermore, many young people mistakenly believe that they do not need life insurance until they have dependents. However, considering the potential for future liabilities and financial responsibilities, obtaining a policy at a younger age can lock in lower rates and provide peace of mind. Educating oneself about these misconceptions can empower young adults to make informed decisions about life insurance products and recognize their importance in safeguarding their financial future.

Planning for the Future: Beyond Life Insurance

While life insurance is an essential component of financial planning, it is crucial to understand that it is not a standalone solution. Young adults in the United States should approach their financial futures with a comprehensive strategy that encompasses various financial instruments, including retirement accounts, emergency funds, and investment portfolios. Integrating life insurance within this broader framework can help ensure long-term financial security.

Life insurance serves primarily to provide financial support for dependents in the event of an unexpected demise. However, its significance extends beyond mere death benefits. When strategically combined with savings tools like emergency funds, which serve to cushion against unexpected expenses, and retirement accounts like 401(k)s or IRAs, life insurance contributes to a robust financial plan. The importance of building an emergency fund cannot be overstated; it acts as a safety net, enabling individuals to manage unanticipated financial burdens.

Investing in retirement accounts early also establishes a foundation for long-term wealth growth. Such accounts often offer tax benefits and compound interest, leading to increased savings over time. Integrating life insurance with these vehicles can further enhance one’s financial strategy. For instance, certain permanent life insurance policies can accumulate cash value, serving as an additional investment resource while still providing necessary life coverage.

Moreover, having a diverse financial approach allows for greater flexibility in managing risks associated with life’s uncertainties. By considering life insurance as part of a financial ecosystem rather than in isolation, young adults can not only safeguard their families but also build a stable economic future. Prioritizing these elements simultaneously—life insurance, savings, and investments—ensures a balanced approach to financial planning and security.

Conclusion: The Case for Early Life Insurance Investment

In reflecting on the importance of life insurance, it becomes clear that young adults in the United States stand to benefit significantly from considering life insurance early in their lives. This financial tool not only provides peace of mind but also ensures a safety net for loved ones, should unforeseen circumstances arise. The discussion has highlighted various advantages, including affordability and flexibility, as life insurance premiums are typically lower for younger individuals compared to their older counterparts.

Additionally, acquiring life insurance at a younger age can enhance financial planning opportunities. By building coverage and investment over time, individuals can secure their financial future more effectively. Furthermore, having a life insurance policy may not only cover unexpected expenses but also provide future financial support for family members, ensuring their well-being during challenging times.

We also touched upon the emotional and psychological relief that a life insurance policy can provide. Knowing that one’s family will be financially protected fosters a sense of security, allowing young adults to focus on their ambitions without the worry of what could happen in the future.

In light of these considerations, young adults are strongly encouraged to explore their life insurance options. Engaging with financial advisors, assessing personal circumstances, and understanding the range of products available can empower individuals to make informed decisions. Investing in life insurance early not only serves as a proactive step towards financial responsibility but also demonstrates a commitment to safeguarding one’s future and supporting loved ones. Therefore, it is imperative to act and unlock the potential benefits of life insurance before the opportunity diminishes with age.